September 29, 2014

In this corner, you, Mr. Individual Investor and your trainer Modern Portfolio Theory. In the other corner, Mr. Market. He doesn’t care about your plan or your theories. Every so often he will try to punch you hard right in your Efficient Frontier. You won’t see it coming. Are you going to wait until you get punched before you change plans? The record shows that you have far lower investment returns than Mr. Market (see http://seekingalpha.com/article/2461815-average-investors-have-no-rhythm).

Summary:

- The prevailing plan of individual investors is to be somewhat diversified and to buy and hold.

- After a six year run-up in prices of risk assets, it may be wise to consider how this strategy will serve you going forward.

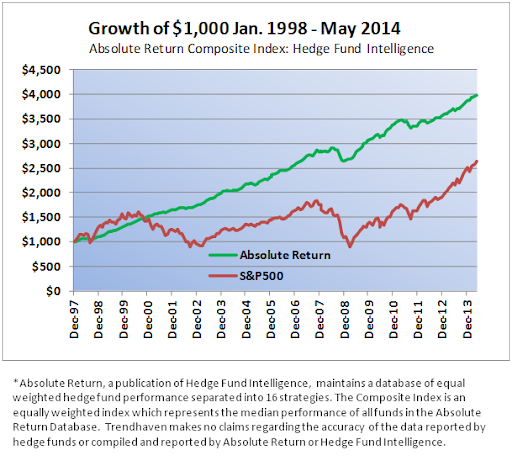

- An alternative approach called Absolute Return, the purview of hedge funds and managed futures, is also available to average investors whose wealth might be permanently impaired if they suffered an extended drawdown of their portfolio value.

There are those who believe that the market for risk assets is near a peak and due for some meaningful correction from its gravity-defying ascent. Others believe that the prices for risk assets like stocks will continue upwards for the foreseeable future and that a correction either won’t come or won’t last long because of the commitment of central banks to protect the economy… and the value of stock markets has become their benchmark for economic health. Maybe they discount the possibility that at some point policy makers will choose, or be forced, not to backstop a fall in market prices. For some, the memory of previous correction/recovery epics may have faded.

- It took 17 months for the S&P 500 to fall 57% in the 2007-2008 financial crisis and 5.4 years to recover (total return). More significantly, recovery took that long with central banks flooding markets with liquidity and forcing money out of savings and into risk assets to find a return.

- It took 30 months for the S&P 500 to fall 49% between late March 2000 and early October 2002, and seven years to recover (total return).

It can be difficult to part with an investment that has, over the last five and a half years, delivered capital gains and dividends that together have far exceeded the investment returns of investment grade bonds or cash. You hate to be out of the stock market, bond yields are terrible and cash pays next to nothing. And if you get out, how will you know when to reenter? After a 10% correction? After 20%? The answer most often proffered is to just stay invested, ride through any correction, and be in the market when it recovers again, as it always does. Buy and hold and stay the course. This is sound advice if:

- You don’t think the market is ever going to have another major correction (a foolish assumption), or

- The resurgence after correction will be swift and thorough (another foolish assumption); or

- You will not have to use any of these funds when you are in drawdown (which depends on your personal situation); or

- You do not have a good way of knowing when to reenter the market if you get out (which, given the advice available from most sources, is a legitimate concern)

If your plan is to manage risk of investment loss via diversification among a variety of asset classes, how did that work out for you in the last major market correction? Many learned that the price movements of different asset classes can correlate to the downside when you most needed them to be negatively correlated. During the last major market correction, the Fidelity Balanced Fund lost 43% during the same period the S&P 500 tanked 57%.

Here is an idea. Consider reallocating into a reliable Absolute Return strategy. Yes, unlike unicorns, they do exist, notwithstanding the lackluster performance of some hedge funds attempting but failing to realize the intent of the strategy. The goal of an Absolute Return approach is to avoid drawdown while delivering a positive rate of return. It is variously attempted mostly with the use of timed market allocations and/or hedged positions. When it works, it will deliver superior and steady long term growth of investment value through market cycles. Find one and you can stay invested in this bull market as long as it makes sense, and have some assurance that you will not bear the full brunt of the next major market correction.

A viable Absolute Return strategy would keep you invested (net long) while the market trends upwards, then diminish your net exposure sometime near the peaking of the up-trend and beginning of a down-trend. Ideally, you should have no net long exposure during most of the down-trend, and finally get back into risk assets somewhere in the trough. If the next major market correction is not followed by a quick recovery in prices, your portfolio should be protected from a premature reentry. With interest rates so low and the Fed’s balance sheet so extended, the duration of the recovery from the next major market correction should be a concern for equity investors. If you are either very wealthy or young, perhaps you are more sanguine. Even so, capturing most of the up-trends and missing most of the down-trends helps your investment returns no matter what your risk tolerance or liquidity needs.

If you are in or approaching retirement, a buy and hold approach applied to risk assets in today’s environment may be ill advised. Risk is the chance of permanent impairment of wealth. Is there a possibility you might have to use some of your investment funds to live on during a 5-7 year drawdown period? If so, you run the chance of locking in losses. Treat the gains you may have made over the last five years as your own. Protect them.

Absolute Return investing has never looked as desirable as it does today. And, it is not a strategy only available to qualified high net worth investors and institutions, or via hedge funds. It is an investment goal also pursued by some mutual funds and separately managed accounts.

Trendhaven is a Registered Investment Advisor offering an Absolute Return approach in a safe, liquid managed account structure. Learn more at www.trendhaven.net.